Summary

- DARA is planning to be acquired by UK-listed Midatech Pharma.

- Midatech’s offer to DARA shareholders consists of ADRs as well as a CVR based on certain milestones.

- After the deal is completed Midatech’s ADRs will start trading in the US.

- Due to lack of institutional interest DARA trades at a 16% discount to Midatech’s offer (excl. CVR).

- DARA’s shareholders will vote on this deal on Wednesday, making this an attractive short term play.

Introduction:

DARA Biosciences (NASDAQ:DARA) is a small specialty pharmaceutical company focusing on the commercialization of oncology treatment and oncology supportive care products. In June of this year DARA announced it had reached a merger agreement with UK-listed Midatech Pharma. Midatech is offering DARA shareholders to exchange DARA shares for newly issued Midatech ADRs.

Seeking Alpha-contributor Daniel Ward wrote an excellent article about a possible merger arbitrage play in DARA Biosciences last July. At that time he pointed out the risks, but concluded DARA shares were undervalued. Now, almost five months later, DARA is trading only slightly up to what it did then. Yet the risks surrounding Midatech’s offer have greatly decreased. With only two days to go before DARA’s shareholders do a final vote on the offer, I believe it’s high time to revisit this opportunity.

The offer:

Midatech’s offer for DARA consists of two parts:

- Shares. Midatech’s offer is for DARA shareholders to exchange their DARA-shares into Midatech ADRs (American Depository Receipts). The exact exchange ratio depends on the average Midatech share price over a period of fifteen days before the offer is completed, as well as the GBP/USD spot rate. Based on the current Midatech share price its bid is worth USD 1.095 per DARA share. Due to the way the deal is structured DARA-shareholders are pretty much guaranteed to receive at least USD 1.08 per DARA share. Upon completion of the transaction the newly issued ADRs will start trading in the US. Every ADR will represent the right to receive two ordinary Midatech shares.

- CVR. Midatech also offers DARA shareholders a Contingent Value Right, also known as a CVR. This CVR entitles DARA shareholders to a maximum payment of another USD 0.18 per share, based on certain milestones with regards to sales in 2016 and 2017 of two of DARA’s products, Gelclair and Oravig. If only some of the milestones are met, there will be partial payment. If none of the milestones are met, the CVR will not pay out anything.

DARA shares currently trade at USD 0.925. This means it trades at a 16% discount to Midatech’s bid, assuming the CVR expires worthless. It trades at a 28% discount to Midatech’s bid, assuming the CVR pays out in full.

About Midatech Pharma:

Midatech Pharma is a UK-based nanomedicine company, which is trying to develop a pipeline of product candidates in development for rare diseases with unmet medical need. It intends to accelerate growth by actively pursuing strategic acquisitions. Midatech is traded under ticker MTPH on the Alternative Investment Market, which is a submarket of the London Stock Exchange with a more flexible regulatory system meant for smaller companies. Midatech, which IPO’d in December of 2014, currently has a market cap of approximately 74 million pound (111 million dollar) and a large institutional ownership base. Only 24% of its shares are in public hands.

The biggest shareholder by far is Woodford Investment Management, which owns a 21.5% stake. This fund, that coincidentally made the news this weekend with regards to its holdings in biotech Northwest Biotherapeutics (NASDAQ:NWBO), has a number of significant holdings in the US as well.

Possible risks:

As always with any merger play it’s important to fully understand the risks. I’ll discuss a few of them below:

Midatech could walk away from the deal

An important risk for every merger is that the acquiring party may withdraw its bid at any time. This deal has a limited break fee, which means it’s relatively cheap for Midatech to walk away.

While this was a significant risk five months ago when Ward wrote his article, this seems extremely unlikely now. Midatech appears firmly committed to completing this deal, as it fits the company’s aggressive acquisition strategy.

On top of this, on the 18th of November Midatech announced it is currently negotiating terms for yet another (unidentified) complementary US acquisition. This acquisition is contingent on completion of its offer on DARA.

DARA shareholders could reject the bid

Next Wednesday DARA shareholders will get the chance to vote on the bid. The company has a limited 11% institutional ownership, with no party holding a 5% stake or over. This makes a vote harder to predict, even though DARA itself recommends accepting the bid.

However, the rationale for voting against the bid doesn’t seem that strong. Per the 30th of September DARA still had 4.6 million dollar in cash, and with limited revenue growth and no positive cash flow in sight it is burning through that cash at a quick rate. It expects to run out of cash in the first quarter of 2016.

DARA shareholders have not been in for a treat those last few years: the share price lost over 90% of its value.

(click to enlarge)

Source: Stock chart DARA, otcmarkets.com. Prices adjusted for reverse split.

The best chance for long term DARA shareholders to recoup some of their losses seems to be to vote for the bid. Midatech says it has sufficient cash to fund its own operations, DARA’s operations, and the operations of the possible second acquisition, for at least the next twelve months.

On top of this Nasdaq is threatening to delist DARA because its share price is not in compliance with the minimum bid price requirement of $ 1.00 per share. A completion of the take-over by Midatech would solve this problem.

Taking all of this into consideration, I find it unlikely the bid will get rejected on Wednesday. It’s worth noting that if the bid does get rejected, the DARA share price does appear to have considerable downside.

After completion of the bid the Midatech ADRs could trade at a significant discount to Midatech Ordinary Shares

DARA shareholders will be paid by Midatech in Midatech ADRs. These ADRs will begin trading in the US, and could potentially trade at a discount to Midatech’s Ordinary Shares in the UK. However, Midatech has already confirmed it will be possible to convert the US ADRs into UK Ordinary Shares on request.

(click to enlarge)

Source: DEFM14A SEC-filing DARA Biosciences

This would create an arbitrage opportunity if Midatech’s ADR would trade at a considerable discount for an extended period of time, and therefore such a discount is unlikely to persist.

The price for Midatech Ordinary Shares could fall, instead of the price for the ADR rising

Midatech’s ADRs trading in tandem with its Ordinary Shares could cause the price of the ADRs to go up, but the same mechanism could obviously also cause the price of the Ordinary Shares in the UK to go down. Because of the heavy institutional ownership and a limited free float, Midatech’s Ordinary Shares are illiquid at the best of times. This means heavy demand could drive down the price across the pond, at least temporarily. It’s definitely a risk worth noting, even though Midatech’s market cap is over five times DARA’s market cap.

The CVR could expire worthless

The CVR paying out in full would offer DARA shareholders a significant additional payout of up to USD 0.18 per share over the coming years. The chance of the CVR not paying out in full, or not paying out at all, appears to be rather large though. Ward wrote in his article “holders are very unlikely to receive any payout from the CVR”.

Midatech’s CEO, Jim Phillips, commented also. He said on a conference call held in June:

So if they [DARA] reach their forecast, the CVR becomes payable, and the CVR is calculated on essentially the difference between our forecast and their [DARA’s] forecast and the gross margin that that contributes.

In other words, Midatech itself doesn’t expect to pay out on the CVR unless sales generated by the DARA pipeline are above its own expectations. It therefore seems prudent to analyze this merger play purely based on the value of the stock that’s being offered, and not based on the potential value of the CVR.

Too good to be true?

Even when ignoring the CVR, a 16% a discount for a deal that seems only a few days away from closing seems too good to be true. Merger arbitrage is generally about low single digit returns. I believe this spread is likely caused by a lack of interest of institutional merger arbitrage funds. The DARA-offer, with an estimated value of about 21.5 million dollar is extremely small compared to the many multi-billion dollar M&A deals currently pending. This will likely not make it worth the effort of taking a position for any large player.

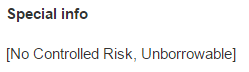

Also, a complicating factor is the apparent impossibility to properly hedge this deal. The share price of the UK-listed Midatech Ordinary Shares falling after the deal closes is a definitive risk, which one could normally easily mitigate by shorting those shares right now. However, shorting seems impossible for everyone in the market place, as the shares just aren’t available for borrow anywhere. I’ve contacted several brokers, including major UK based brokers: none have a borrow available.

Source: IG.com, details for Midatech Pharma

Euroclear, through UK-based securities settlement system CREST, reported a short interest in Midatech for October 2015 of only 10.000 shares, which is 0.03% of the total number of shares outstanding.

Source: Euroclear. October 2015 stock loan data.

With institutional merger arbitrageurs out, this leaves only retail investors, who might not completely understand the value of Midatech’s offer. The offer is rather difficult to comprehend, based on a floating share exchange rate and further influenced by several other factors. On top of this, it might not be clear to all DARA-shareholders they will receive US-listed Midatech shares, rather than UK-listed ones. Finally, Nasdaq’s Notice of Delisting might have further scared off some participants, even though the threat of a delisting will be off the table once the transaction succeeds.

Conclusion:

I believe, at current prices, investment in DARA offers an attractive merger play to investors. The size of the discount with which DARA is currently trading versus the value of the offer by Midatech Pharma of approximately 16%, excluding a CVR, is sizable. Part of this spread can be explained as there are risks involved which, as described in the article, cannot be hedged. Nevertheless, in my opinion the risk/reward is favorable.

If DARA shareholders approve the deal on Wednesday, the transaction will likely close soon after. This, barring any unforeseen circumstances, will make this a short term play with capital tied up for only a limited period of time.

Disclosure:

I am long DARA through an owned entity. I have no business relationship with any of the companies mentioned in this article. This article is not an advice to either buy or sell; it expresses my own personal opinion.