Summary

* Ten OTC-listed stocks appear independent, but are run by a small group of insiders.

* These insiders net millions on convertible debt conversion at the expense of shareholders.

* CEOs appear to be puppets on a string; voting majority is hidden in Panama.

* ASCC, CHGT, FTTN, GTSO, MYGG, NTRR, OMVS, RBCC, SGNI and TAYO are all worth zero.

The Titanic Ten

At first glance Aristocrat Group (OTCQB:ASCC), Changing Technologies (OTCQB:CHGT), First Titan (OTCQB:FTTN), Green Technology (OTCQB:GTSO), MyGo Games (OTCQB:MYGG), Neutra Corp. (OTCQB:NTRR), On The Move Systems (OTCPK:OMVS), Rainbow Coral (OTCQB:RBCC), StemGen (OTCQB:SGNI) and Taylor Consulting (OTCQB:TAYO) have nothing in common. These are ten OTC-listed companies, mostly located in different parts of the US. All have (or claim to have) wildly different activities.

(click to enlarge)

In this article, I’ll argue shares in all of these companies, referred to them as the Titanic Ten for the remainder of this article, are in fact worthless.

I’ll briefly discuss every single one of the Titanic Ten, but I’ll also show how these companies can all be tied together and how their corporate actions can be attributed to the interests of only a few individuals. These individuals have no interest in actually seeing any of these ten companies succeed: they are only interested in using them as a printing press of a never-ending stream of new shares which they continuously dump in the open market. When the share price is eventually run into the ground, a reverse split is done and the whole cycle repeats itself once more.

In this article, I’ll identify the individuals behind this scheme, as well as the way they operate.

The Titanic Ten all appear to be nano-cap stocks, with market caps of anything up to $20 million. This picture changes completely when taking into account potentially convertible shares from outstanding debt agreements (more about that later) that can be converted at any time. Including those potential shares, OMVS, for example, is worth over $500 million. ASCC is worth over $300 million. Remarkable valuations for companies with none or hardly any revenue whatsoever.

Link #1: Massive toxic convertible debt

The Titanic Ten all have large amounts of convertible debt on their balance sheets. Because all of the companies are very low on cash, they use advances from a third party to pay the bills. Then, usually once per quarter, these advances are converted into convertible notes. The notes generally bear interest of around 10% per year. The main attraction of the notes however is they are convertible into stock at a fixed conversion price per share.

This convertible debt is always issued at a hefty discount to the current share price, making it attractive for that third party to immediately convert the debt and dump the shares for a nice profit in the open market. That’s not all though. In a previous article, I wrote on Seeking Alpha about GTSO I showed a clause in the terms of the convertible debt forbidding adjustment of the conversion price in case of a reverse split of the underlying shares.

(click to enlarge)

Source: 8-K SEC filing Green Technology Solutions

When a reverse split is done, the share price of a stock increases proportionally. For example, in case of a 1-for-200 reverse split, every shareholder will receive one "new" share for 200 "old" shares. A $0.01 share price for the "old" share will therefore increase to a $2.00 share price for the "new" share.

It’s common practice to also adjust the conversion price of all convertible debt (see recent example). Otherwise, holders of convertible debt would make a windfall when the conversion price of their debt suddenly becomes a fraction of the current share price. And this is in a nutshell exactly what happened when five (ASCC, FTTN, GTSO, OMVS and RBCC) out of the Titanic Ten did a reverse split in the last twelve months. In all of those cases, the conversion price of the debt was not adjusted.

In my previous article on GTSO, I calculated how not adjusting the conversion price of convertible debt after a reverse split in September 2014 made holders of GTSO-debt almost $2.5 million in six months. As a result of debt being converted to shares on a very large scale after the recent reverse split, the total number of outstanding shares GTSO increased over 2,000% since September last year. It’s no surprise over that same period the share price lost 95% of its value.

The table below demonstrates what an enormous effect not adjusting the conversion price has on the equity structure of a company. The table shows the five companies that recently did do a reverse split as well as the five that didn’t reverse split, with the total number of shares outstanding according to their latest SEC filings. Next to it are the number of potential shares that can be created from the conversion of debt, as well as the conversion price range.

(click to enlarge)

The companies that didn’t recently do a reverse split have quite a significant overhang of convertible shares. For example, MYGG’s share capital would grow over 50% if its current convertible debt would all be converted into shares. However, this is nothing compared to the companies that did do a reverse split recently. ASCC and OMVS have over 170 times potential new convertible shares compared to their current number of common stock. FTTN has an overhang of over 90 times the current number of shares outstanding. In comparison, GTSO and RBCC almost look normal with eighteen and three potentially convertible shares for every one share currently outstanding. There’s nothing normal about this situation though.

The table also shows these convertible shares can be converted to common stock at prices which are in many cases over 99% below the current share price of the company. The only restriction in converting debt into shares is the debt holder is not allowed to at any point hold more than a 4.99% stake in any company. This restriction effectively means the debt holder needs to constantly dump shares in the open market to be able to convert even more additional debt.

This cycle has an obvious negative effect on the long-term share price. Constant dumping depresses the price over and over again.

(click to enlarge)

Source: Stock chart FTTN, www.otcmarkets.com. Prices adjusted for reverse split.

Knowing this it’s no wonder shares in, for example, FTTN, a supposed oil and gas exploration company, returned a negative yield of 99.7% over the last three years. Also, knowing this, it’s not hard to predict FTTN will again lose 99% of its value over the next three years, as will the other nine other companies featured in this article.

It’s quite clear: debt holders are making a fortune on the back of shareholders. Which brings us to the obvious question: who are these debt holders exactly? Let’s take a look at some recent filings:

Source: 10-Q SEC filing On The Move Systems Corp

Source: 10-K SEC filing Rainbow Coral Corp.

Source: 10-K SEC filing Taylor Consulting

Vista View Ventures, a company owned by an individual named Thomas Cloud, pops up as a buyer of convertible debt in relation to almost every company of the Titanic Ten. KMDA Consulting, owned by a Houston attorney named Kathleen Delaney, seems to typically provide "middle-men" services.

Vista View isn’t the only company buying debt though. MYGO disclosed it has sold toxic convertible debt to a company called Montego Blue, owned by Monika Federowicz. ASCC disclosed it has made a deal that allows the Jaxon Group, owned by John Morrissey, to buy $5 million worth of stock at a 50% discount to the current stock price of ASCC. Both Montego Blue and Jaxon, as well as THM Consulting, owned by Thomas Morrissey, also turn up in connection with a recent share offering by SGNI.

It’s probably important to note Kathleen Delaney, John Morrissey and Thomas Morrissey are all related to each other. Also, Monika Federowicz is the wife of Robert Federowicz, the CEO of ASCC. I’m sure you start to get a picture of what’s going on. At the top of the food chain, a very small inner circle of people seems to be calling the shots at the Titanic Ten, making sure they walk away with the profits while shareholders are left behind holding the bag.

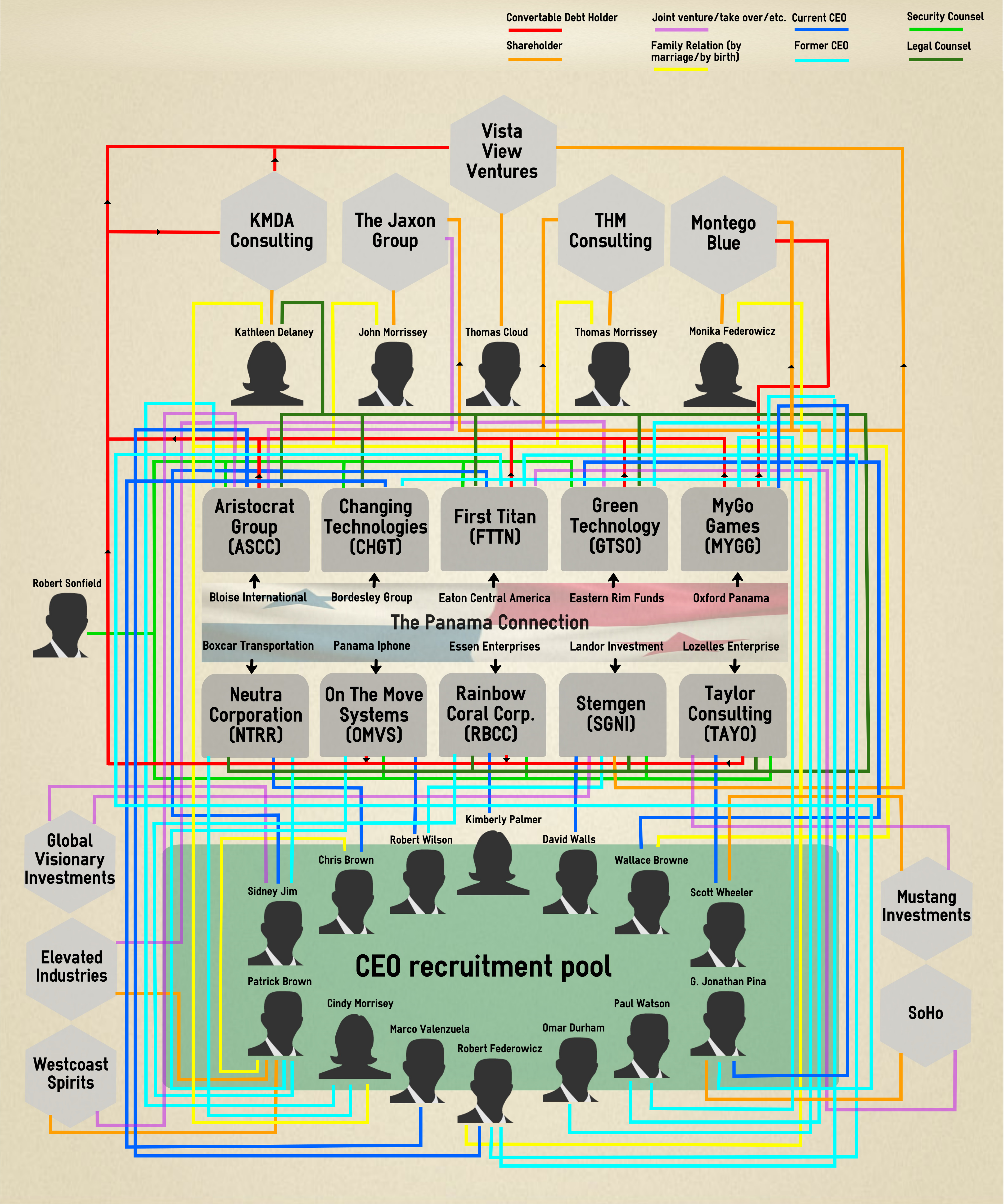

The diagram below shows the ties between the Titanic Ten and the debt- and share-holders. Please note, it only shows the ties I could conclusively verify based on (mostly) SEC filings and other sources.

(click to enlarge)

Link #2: The CEO recruitment pool

There’s a second factor that ties the Titanic Ten together, and that’s the CEOs. Because, if all of those convertible notes are that bad for the company and its shareholders, why would any Board of Directors of any company approve it? Don’t they have a fiduciary duty to shareholders?

Well, in most cases, the Board of Directors consists of only one person. And to make matters worse, this one person appears to have been selected not because of his/her skills, but purely based on his/her social contacts. All of the CEOs are family or friends of the "inner circle" I described previously. Also, CEOs routinely get moved around. Many of the current CEOs of any of the Titanic Ten have served one or multiple terms as CEO with another company in the past.

I have edited the diagram to show what I’ll call "the CEO recruitment pool". This pool consists of fourteen individuals who all seem to take turns serving as CEO for one of the Titanic Ten companies.

(click to enlarge)

Taking into account the way CEOs are recruited, the background of, for example, the CEO of RBCC might not come as such a big surprise. RBCC is a company that claims to have been formed to grow, harvest and distribute coral. Ironically, the only revenue the company seems to generate comes from one small Florida-based fishing equipment shop it owns on the side. Its CEO, Kimberly Palmer, is a registered nurse who, according to her Facebook profile, lives in Vancouver, Canada. Miss Palmer appears to have no affinity with coral whatsoever and is living over 3,000 miles away from where the company is supposed to be operating from. Yet, she is paid 60,000 USD a year. Most likely for looking the other way and doing absolutely nothing while RBCC shareholders are wiped out on her watch.

Not only Kimberly Palmer is active on Facebook, but also most of the CEOs have profiles there and, surprisingly, are pretty lax with their security settings. Therefore, it isn’t difficult to spot almost everyone in the pool is Facebook pals with another either directly or indirectly. They even comment on each others’ pictures. A great example of this is the picture below:

(click to enlarge)

Source: Facebook.com

This photo was taken from the Facebook page of Sidney Jim. Sidney is among others’ Facebook friends with Thomas Cloud, the person behind Vista View Ventures. Sidney is also the former CEO of NTRR (company #1 from the Titanic Ten), the current CEO of FTTN (company #2), and in all of this has found the time to act as a registered agent for a supposed consultancy business that was sold to SGNI (company #3). On this picture he’s driving around on a race track in a very cool looking personalized sports car, which is clearly sponsored by RWB Vodka. RWB Vodka is a brand that, you guessed it, is owned by ASCC (company #4). It’s not a big mystery who likely paid for Sidney’s car here: the ASCC shareholders.

As you can see in the picture, David Walls, who is the current CEO of SGNI, liked Sidney’s pic. He comments "Bad Ass!!"

Link #3 The Panama connection

Previously, I explained why the CEO of these companies do not intervene while their companies are being buried under toxic debt. One might also wonder why the shareholders don’t act. For example, a reverse stock split needs to be approved by a voting majority. If shareholders know the disastrous effect of such a reverse split on the capital structure of the company, why don’t they object? This is because they can’t: the voting majority is safely stacked away somewhere in Panama.

(click to enlarge)

As can be seen above, The Titanic Ten can all be linked to a Panamanian counterpart, who maintains a voting majority to approve every resolution that needs approval. Or, if that voting majority is lost because of the constant share dilution, even more convertible debt is created and issued to those Panamanian companies to again ensure a voting majority right in time for every vote. See below for an example:

(click to enlarge)

Source: 10-Q SEC filing First Titan

There’s also a more drastic solution to make sure the voting control isn’t diluted along with the common shares: by in effect removing the voting rights from the common shares altogether. An increasing number of the Titanic Ten have created a special set of preferred shares: these shares have been practically given away to their Panamanian shareholders. The preferred shares generally have superior voting rights to the common shares, providing the holders of the preferred shares with a complete power to approve any resolutions coming from the board without opposition. See below:

(click to enlarge)

Source: 10-K SEC filing Green Technology Solutions

The fact all of these "controlling" companies come from Panama is no coincidence. Panama allows companies to keep information about owners and directors confidential and does not keep this information on public record.

Link #4: Takeovers, joint ventures and generic PR

If you want to pretend to the public you are a company of some size while you’re actually not, it’s obviously important to fake the things actual companies are doing for real. So that means you need to send out press releases, do actual takeovers and create joint ventures to appear to be seriously pursuing your business goals.

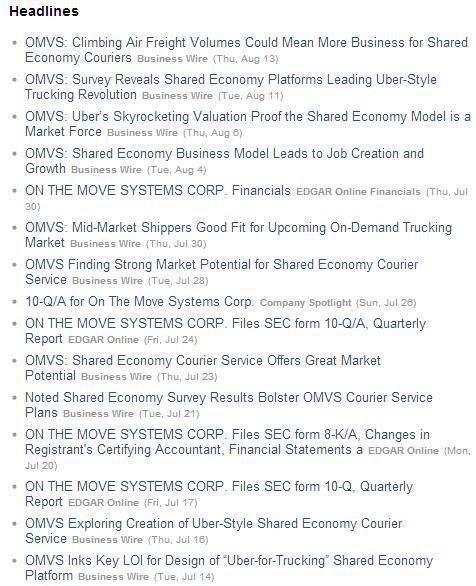

Let’s talk about press releases first. This is something the Titanic Ten are very, very good at. An endless stream of generic PR is sent out every week. OMVS is a good example of this. The OMVS business model is rather remarkable: it says it intends to create an app to help truckers and, as such, mysteriously claims to be comparable to taxi-app Uber. However, to be perfectly clear, OMVS hasn’t created an app yet, and doesn’t even seem to have done anything to create one. Yet, several times a week the company sends out a press release about the trucking industry in general, its enormous size and growth potential, and any future developments that might have an impact. For illustration purposes, I’ve included a screenshot of the latest headlines of the most recent OMVS press releases: I’m sure you’ll get my point based on the headlines alone.

Source: Yahoo Finance

Another fine example is TAYO. This real estate development company regularly boasts when it has made a real estate sale using terms in its press releases like "windfall", "expands revenues" and "revenues continues to climb". Yet, in its latest 10-K filing, TAYO admitted having realized only $33 thousand in revenue for the latest full year, of which only $14 thousand was actually generated by any real estate sales. The TAYO real estate portfolio really seems to solely consist of a few storage units and 48 unimproved lots located somewhere in Texas, bought for a grand total of $65 thousand.

A third company of the Titanic Ten, CHGT, has also been very busy making a name for itself. This company, which claims to specialize in 3D printing, made so much noise it even attracted the attention of industry insiders. 3DPrintingIndustry.com is a leading website dedicated to reporting on the latest developments in the world of 3D printing. It wrote several blog-articles on CHGT (here, here, here and here) basically exposing the company as a complete fraud.

Sending out generic press releases on no-news events is one thing, but actually having to do takeovers and building joint -ventures is quite another. Obviously, to do such a transaction you need a real counterparty. Well, the companies the Titanic Ten are buying, or cooperating with, really do exist. Even though most of the time they are suspiciously recently incorporated. These companies are registered in a large variety of different US states and sometimes even abroad. Unfortunately, it’s not always straight forward to trace the individuals who are behind those companies.

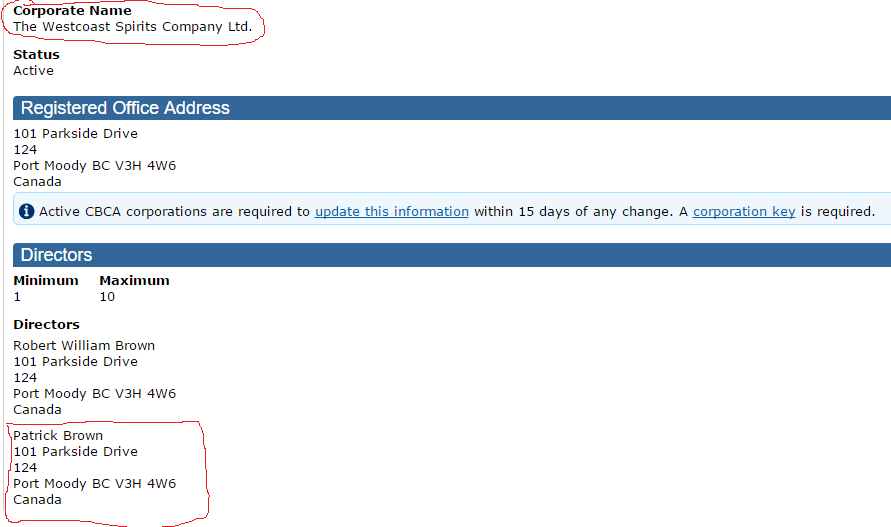

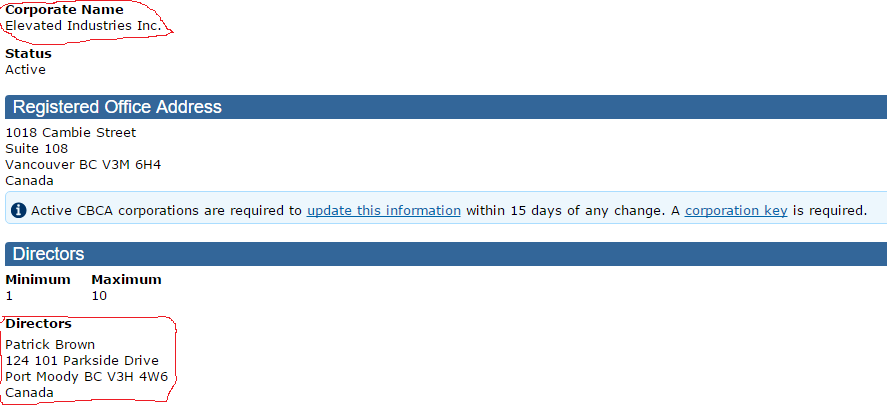

However, as it turns out, in Canada, it is actually quite easy to find out the names of the directors of a privately-held company. This is a fortunate coincidence as both ASCC (the company that tries to sell its own brand of vodka mentioned earlier in this article) and GTSO (a company whose mission is to "support and the health and wellness sub-market of medical cannabis") have announced joint ventures with Canadian companies to pursue the Canadian market in their own line of activity. ASCC announced a distribution agreement with The Westcoast Spirits Company, GTSO first announced a joint venture with Elevated Industries, then later announced its intent to buy Elevated altogether. A quick search on both these companies turns up the following:

Source: www.ic.gc.ca/

Both Westcoast Spirits, and Elevated Industries have the same director, a man called Patrick Brown. In itself a remarkable coincidence as Westcoast is supposed to be a spirits distributor while Elevated Industries claims to be a company "that owns unique formulations for frozen confections infused with cannabis extracts".

Of course all of this isn’t a coincidence: Patrick Brown isn’t just a random person: he’s actually a prominent member of the CEO recruitment pool I mentioned earlier. Brown has in the past served as CEO of both OMVS and RBCC.

All of this raises a hefty suspicion the announced deals are mostly fake. The companies used in partnerships are held by insiders, with the sole purpose of creating an illusion that something is happening. A company that basically does nothing buys or starts a joint venture with another company that does nothing; and all of this to entice investors into buying worthless shares.

Link #5 Securities & legal counsel

It’s probably no surprise the previously mentioned Kathleen Delaney, who appears to play a central role in all of this, acts as legal counsel for eight out of ten companies featured in this article. Despite a somewhat blemished past, Robert Sonfield Jr. has also been chosen as securities counsel by at least eight out of ten companies.

Taking these two final links into account, I was able to come up with the final version of the diagram linking the Titanic Ten firmly together.

(click to enlarge)

MYGG: The one that almost got away

The Titanic Ten came very close to being only nine. In the spring of 2014, MYGG, a gaming developing company, seemed very much like the other nine companies featured in this article. The company had the usual convertible debt on its balance sheet, and its CEO, Paul Watson, had previously served as the CEO of GTSO.

Yet, in 2014, the inner circle of debt holders seemed to have temporarily lost control of the company when MYGG, through a share exchange, bought another gaming development company called Great Outdoors. In this transaction, the owner of Great Outdoors, Daniel Hammett, obtained a 71% majority in MYGG and became the new CEO.

There was one problem though. Hammett wasn’t an insider: he has a strong background in the gaming industry, having worked at, among others, Activision (NASDAQ:ATVI) and Vivendi Universal. Hammett must have quickly realized there was something terribly wrong with the balance sheet of the company he had just become CEO of.

In July 2014, MYGG filed a 10-Q with the SEC that contained the following remarkable paragraph:

(click to enlarge)

Source: 10-Q SEC filing MyGo Games Holding

Hammett appears to have tried to cut the ties between MYGG and Kathleen Delaney by openly disputing the amounts owed. He must have realized MYGG would be doomed to fail, unless the toxic convertible debt would be renegotiated.

Two months later, Hammett was gone, after he was accused by the company of breaching MYGG’s Code of Business and Ethical Conduct. In October, Hammett reached a settlement with MYGG with regards to his departure, which included returning his stake.

Hammett was quickly replaced by Jonathan Pina. With Pina being named the new CEO, everything seems to have gone back to normal at MYGG. Pina has, as we’ve learnt to expect, no relevant working experience in the gaming industry, and previously served as the CEO of FTTN, another Titanic Ten Company. Not surprisingly MYGG never did a follow up on its dispute of the amount it owed to KMDA and other counterparties. It’s also no surprise those toxic debts are still present today on MYGG’s balance sheet.

And the story goes on…

Five out of the Titanic Ten did a reverse split in the last twelve months. Number six is on its way: NTRR is a company that wants to market and participate in the market for nutraceutical natural medicine. It never generated any revenue. On the 14th of September, it will hold a special meeting of stockholders in Houston. On the agenda is 1:50 reverse stock split, as well as an authorization to start issuing preferred stock.

Per its latest SEC filing, NTRR has approximately 51 million shares outstanding (although by now this number will no doubt have increased). After the 1:50 reverse split, this count should be reduced to roughly 1 million shares.

In the mean time, convertible debt holders sit on a debt that can be converted into an estimated 9.5 million shares. As with the previous reverse split of the other Titanic Ten, I’m convinced the conversion price of the debt won’t be adjusted. After the reverse split, debt holders will therefore own a potentially convertible 9.5 times the entire total share count.

NTRR is currently trading at approximately 4 cents per share. After the reverse split it will therefore be trading at approximately 2 dollars per share. Shortly after the split, debt holders will no doubt start converting debt to common NTRR stock at prices ranging from 2 to 5 cents per share. They will dump their newly obtained shares in the open market as fast as they can.

Possibly, as also happened with ASCC, GTSO and OMVS this year (see below), a stock promotion will be launched to attract buyers and generate liquidity for a limited amount of time to make sure the NTRR stock price doesn’t immediately implode.

Source: ASCC stock promotion Penny Stock Grower 7-30-15

Source: GTSO stock promotion SmallCapVoice 7-8-15

Source: OMVS stock promotion Penny Stock Chief 7-30-15

As these promotions will die out, the NTRR share price will quickly drop in the months after the split. Shareholders will have lost their shirt yet again while debt holders will have made up to a quick 9,900% return on their original investment.

Conclusion

Let’s face it: most investors investing in OTC-listed stock don’t do so because these companies have rock-solid balance sheets. They do so because they like the sector the company is operating in and believe in its future. The Titanic Ten seem to cater to these kinds of investors very well: you have a cannabis-stock, an app-stock, a "go green"-stock, a vodka-stock, you name it. It’s important to realize the performance of none of these companies is even remotely related to the sector it is in, or the business activities (if any) it initiates. Even if you believe (which I don’t) one of these companies have a bright future ahead in terms of profitability, the shareholders will never get their hands on any of it. The way the Titanic Ten have been financially structured means shareholders will always lose, and holders of the convertible debt will always win.

In this article, I’ve showed several companies with over 100 times the current amount of shares outstanding in potential convertible shares. Even the share price of a solid Wall Street blue-chip stock would collapse under such a weight, let alone a micro-cap company with a questionable business model.

I believe the true value per share of the Titanic Ten (ASCC, CHGT, FTTN, GTSO, MYGG, NTRR, OMVS, RBCC, SGNI and TAYO) is zero. Therefore, I am (long-term) short several of the Titanic Ten companies, see disclosure. The difficulty of finding a short varies per ticker and differs per week. Initiating a short should only be attempted by those who are able to hold on to their positions during temporary volatility caused by stock promotions. Stock promotions in general create excellent entry points to such a short.

When the share price of any of the Titanic Ten will eventually reach zero or close to it, it will just do yet another reverse split. History will simply repeat itself for yet another cycle, wiping out yet another group of investors.

I firmly believe the Titanic Ten should be shut down by the SEC for, among others, a complete disregard of these companies towards its fiduciary duty to its shareholders. I have sent a copy of this article to the SEC for review.

I have contacted MyGo Games, Neutra Corp., Taylor Consulting and Changing Technologies for further information. They did not respond to my request.

I owe credit to Investorshub-poster "Voices of Reason". His/her posts over the years on Cloud, Delaney and others proved invaluable to my research for this article.

Disclosure

I am short ASCC, OMVS, RBCC and SGNI through an owned entity. I have no position in any of the other stocks mentioned, but may initiate a short position over the next 72 hours.